What Is RWA Tokenization? Real World Assets on the Blockchain Explained

by Heidi Chakos

by Heidi ChakosReal world asset (RWA) tokenization is the process of creating a digital representation of a physical or traditional financial asset, such as property, gold, or bonds, on a blockchain. Each token represents a verifiable ownership stake in that underlying asset, making it tradeable, divisible, and programmable in ways the original asset never could be. |

Most of the world's wealth is locked up. Not hidden under mattresses or stashed in offshore accounts, but locked up in the structural sense.

Real estate that can only be bought whole. Fine art that lives in a vault. Private credit markets that simply don't exist for ordinary investors.

The machinery of traditional finance was built for institutions and the super-rich, and the friction it creates is a feature for insiders and a wall for everyone else. Slow settlements, high minimums, opaque ownership records, geographic restrictions: these are not accidents of history. They are the architecture.

Blockchain technology has spent its first decade largely building parallel financial infrastructure for native digital assets. Now, something more ambitious is underway: using that infrastructure to represent assets that already exist in the physical and financial world.

RWA tokenization is what happens when that infrastructure finally turns outward.

What You'll Learn

What RWA tokenization means — not just the dictionary definition, but the mechanics of how a physical asset becomes a blockchain token with real legal standing.

Why this matters for ordinary investors — how fractionalization and global access are quietly dismantling barriers that have kept entire asset classes off-limits for most people.

How the process works end-to-end — from asset origination and legal structuring through to smart contract deployment and secondary market trading.

Which asset classes are already being tokenized — concrete, live examples across real estate, commodities, debt instruments, and more.

Where the real risks lie — the regulatory uncertainty, custody questions, and smart contract vulnerabilities that the hype tends to skip over.

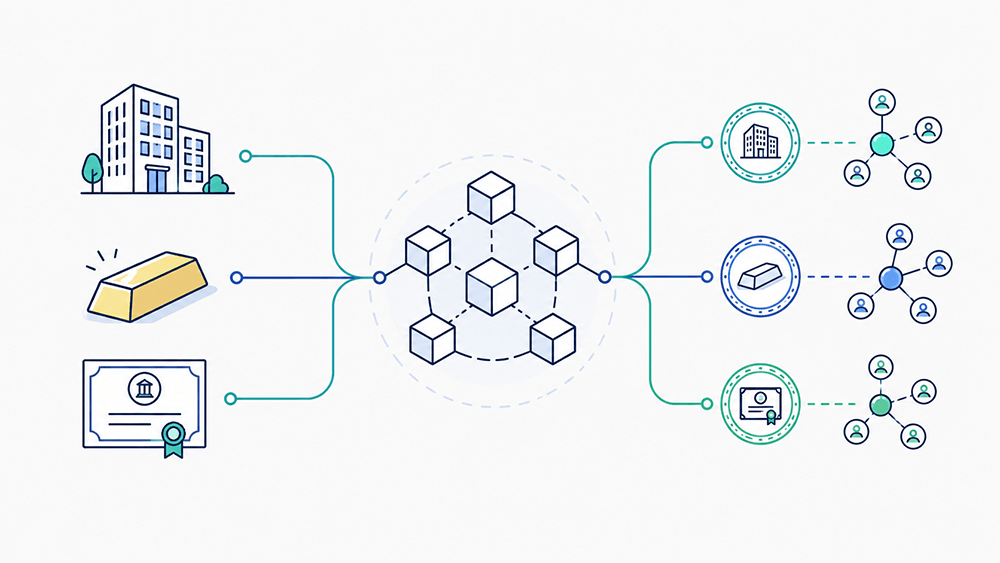

What Are Real World Assets in Crypto?

RWA is shorthand for real-world assets. In a crypto context, it refers to assets that exist outside the blockchain - property, government bonds, gold, invoices, private loans, fine art - that have been brought on-chain through tokenization.

The token itself isn't the asset. That distinction matters more than it sounds.

When you hold an RWA token, you're holding an on-chain representation of a claim on something that exists off-chain. That claim might mean fractional ownership, entitlement to cash flows, a redemption right, or a lien on collateral. What it means exactly depends on the legal structure behind the token - the contracts, the custodians, and the jurisdiction.

So, a useful working definition: an RWA token is an on-chain record of rights to an off-chain asset, enforced by legal and operational structures that exist outside the blockchain.

Tokenization is the process. RWAs are the category of what's being tokenized.

RWAs vs Crypto-Native Tokens

RWA Tokens | Crypto-Native Tokens | |

What backs them | A real-world asset (bond, property, gold) | Nothing off-chain value comes from the network itself |

Examples | OUSG, PAXG, BlackRock BUIDL | BTC, ETH, UNI, SOL |

Legal structure | Typically require custody, KYC, and legal wrappers | Usually permissionless |

Regulatory treatment | Often classified as securities | Varies - often utility or commodity |

Yield source | Underlying asset (interest, rent, dividends) | Protocol rewards, speculation |

Crypto-native tokens originate on-chain. RWA tokens are blockchain representations of something that already existed in traditional finance. The difference shapes everything - how they're regulated, how they're valued,

How RWA Tokenization Works

There's a lifecycle to this. An asset doesn't just appear on-chain. There's a chain of legal, operational, and technical steps that connect the physical world to the blockchain, and every link in that chain matters.

The Tokenization Process Step by Step

Asset selection and valuation. The issuer identifies an asset suitable for tokenization and gets it valued. For real estate, that means appraisals. For private credit, it means underwriting. The quality of this step determines whether the token has any real-world integrity behind it.

Legal structuring. This is the most important layer. The issuer typically creates a legal wrapper - an SPV (special purpose vehicle), a trust, or a fund vehicle - that holds the asset or rights to it. The token then represents a defined claim on that structure. No legal wrapper, no real-world enforceability.

Custody arrangements. Someone has to hold the underlying asset. A custodian safekeeps it, handles servicing (collecting payments, managing defaults), and provides attestations that the asset exists and matches what the tokens claim. Weak custody is where many RWA projects fall short.

Token issuance. The token is minted on a blockchain. Depending on the asset and jurisdiction, transfers may be permissioned (requiring KYC and whitelisting) or more open. The smart contract encodes the rules: who can hold it, under what conditions it transfers, and how redemptions work.

Primary offering. Investors go through KYC and AML checks, then subscribe through a regulated platform. Some offerings are restricted to accredited or institutional investors. Some are open to retail.

Secondary trading. Where permitted, tokens trade on regulated marketplaces or via issuer-approved transfer mechanisms. Smart contract rules enforce compliance automatically - a transfer only settles if the receiving wallet meets the eligibility criteria.

Ongoing management and redemption. Interest payments, reporting, corporate actions, and redemptions are managed through the lifecycle. Redemption is where the on-chain-off-chain connection gets tested. It's also where problems tend to surface first.

Example: How a Rental Property Becomes an RWA TokenA company buys or controls a rental property through a legal structure, such as an SPV. The property is professionally valued, placed under custody or management, and the rights to rental income are defined in legal documents. Tokens are then issued to represent claims on that structure. Investors who hold the tokens may receive rental income, while the token can potentially be traded on an approved marketplace. |

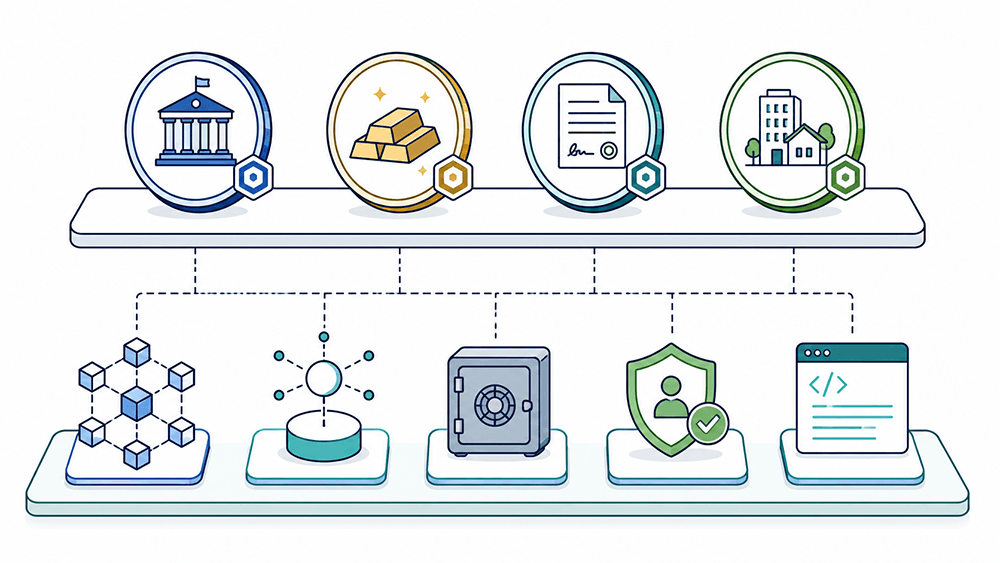

What Gets Tokenized? The Main Asset Classes

The asset class shapes everything - the risk, the yield, the liquidity, and what can go wrong

Asset Class | What Gets Tokenized | Real Example | Key Risk |

Government debt | T-bills, money market exposure | BlackRock BUIDL, Ondo OUSG, Franklin BENJI | Issuer/custodian risk, redemption gating |

Private credit | Loans, invoices, receivables | Centrifuge, Maple Finance | Borrower default, underwriting opacity |

Commodities | Gold, silver, oil claims | PAXG, XAUT (Tether Gold) | Storage/attestation, redemption limits |

Real estate | Fractional property ownership | RealT (US rental properties from ~$50) | Appraisal risk, liquidity mismatch |

Equities and ETFs | Tokenized stocks and funds | Ondo tokenized stocks on Solana, Robinhood EU | Regulatory classification, market hours |

Carbon credits | Emission offset ownership | Various climate protocols | Verification integrity, double-counting |

Private credit is currently the largest segment by far. Active on-chain private credit exceeded $18.9 billion as of late 2025. Tokenized US Treasuries crossed $10 billion for the first time in February 2026. Gold-backed tokens PAXG and XAUT dominate commodities, which rose 289% to reach $5.5 billion by Q1 2026.

Why Crypto Investors Should Pay Attention

This is where it gets really relevant for you.

Most crypto portfolios are heavily correlated. When Bitcoin drops, altcoins drop harder. RWAs offer something genuinely different: exposure to assets that move on their own logic - interest rate environments, credit cycles, commodity supply - not crypto market sentiment.

Fractional ownership changes the maths

A commercial building in Miami, a portfolio of US Treasury bills, a slice of a private credit fund - these were institutional-only plays. Minimums in the hundreds of thousands. Geographic restrictions. Months of paperwork. Tokenization cuts all of that. Platforms like RealT let people buy into US rental properties for as little as $50, receiving rental income in stablecoins. Ondo's OUSG gives anyone access to BlackRock's short-term Treasury ETF through a crypto wallet.

Yield on idle capital

One of the biggest drivers of RWA growth in 2025 and 2026 has been straightforward: people holding stablecoins wanted a return. With US Treasuries generating 4.5–5.3% annualised returns through 2024 into 2025, tokenized Treasury products offered crypto-native investors a way to earn real yield without leaving the blockchain.

24/7 trading and programmability

Traditional bond markets close. Real estate markets are glacial. Tokenized versions of these assets trade around the clock and can be plugged into DeFi protocols as collateral, used in automated yield strategies, or integrated into smart contract logic in ways the original asset never could be.

Portfolio diversification

Adding RWA exposure to a crypto portfolio introduces assets with different risk drivers. Tokenized gold doesn't care about Ethereum gas fees. A private credit pool backed by SME receivables isn't correlated to BTC price. For anyone thinking seriously about portfolio construction rather than pure speculation, that's meaningful.

The Numbers Behind the Growth

The RWA tokenization market has moved fast. Faster than most people in crypto expected.

At the start of 2025, the total tokenized RWA market (excluding stablecoins) was measured in single-digit billions. By early 2026, it was in the tens of billions, with some analytics platforms placing it significantly higher depending on methodology. The trajectory is the point, not the exact figure on any given day.

Long-term projections are more stable and arguably more interesting. BCG's base case puts the tokenized asset market at $16 trillion by 2030 - roughly 10% of global GDP.

Ripple and BCG's joint forecast goes to $18.9 trillion by 2033.

McKinsey is more conservative at $2-4 trillion by decade's end. Even the bearish scenario represents a market that dwarfs anything crypto has built so far.

On the institutional side, the signals are hard to ignore. The New York Stock Exchange announced plans in early 2026 to build its own 24/7 tokenized securities trading platform.

Robinhood deployed over 200 tokenized stock and ETF products for European markets. Goldman Sachs and BNY Mellon are running tokenized money market fund pilots.

For current market size and live data, RWA.xyz tracks the sector in real time.

Who's Building in RWA Right Now

The RWA stack has two layers: the products people hold, and the infrastructure that makes them function.

Products and platforms

BlackRock BUIDL - The largest tokenized money market fund on a public blockchain, offering short-duration Treasury exposure. Over $2.3 billion in tokenized value as of late 2025. The benchmark for institutional-grade on-chain yield.

Ondo Finance (ONDO) - Leads in tokenized Treasury distribution. Its OUSG product wraps BlackRock's BUIDL and crossed $500 million in AUM in early 2026. Also rolling out tokenized stocks and ETFs on Solana. OUSG can be used as DeFi collateral - something a physical T-bill can't do.

Franklin Templeton BENJI - Tokenized government money fund, expanded across multiple networks, including Stellar and Polygon.

Centrifuge (CFG) - The longest-running RWA infrastructure play. Focuses on tokenized private credit and institutional fund structures. Over $2 billion in tokenized assets deployed across 7 chains, with integrations into Aave, Sky, and Morpho.

Maple Finance (SYRUP) - On-chain asset manager focused on institutional lending and credit pools. Professionally managed, underwritten lending with on-chain transparency. SYRUP replaced the older MPL token.

PAXG / XAUT - The two dominant gold-backed tokens. Each represents one troy ounce of physical gold held in custody. Combined, they account for over 80% of the tokenized commodities market.

Infrastructure

Chainlink (LINK) - The oracle backbone of the entire RWA ecosystem. Feeds off-chain data - asset prices, proof of reserves, and NAV calculations - into smart contracts. Without reliable oracles, RWA tokens can't function. Chainlink's Proof of Reserve is already used by major tokenized fund issuers.

Pendle - Enables yield tokenization. Users can separate and trade the yield component of RWA products independently, creating more sophisticated yield strategies.

Newer entrants to watch:

MANTRA (OM) - Compliance-focused Layer 1 built specifically for tokenized assets.

Plume (PLUME) - Infrastructure-first project built around bringing RWAs on-chain and making them usable across DeFi.

Superstate - Founded by former Compound developer Robert Leshner. Regulated fund vehicle designed for crypto-native investors who want Treasury exposure without off-chain account relationships.

Real World Asset Risks

As exciting as RWA tokenization is, this section is a must-read if you want to know both sides of the story.

Legal and Regulatory Uncertainty

Token transfers and legally recognized ownership transfers are not the same thing. In many jurisdictions, the enforceability of a tokenized claim remains untested.

Regulatory frameworks differ sharply by region - the US treats most tokenized securities under existing securities law, Singapore and Hong Kong operate hybrid digital-asset frameworks, and many markets are still in sandbox mode.

IOSCO's 2024 report on decentralized finance flagged this directly: the legal rights attached to tokens must be clearly defined with respect to ownership, transferability, and investor protections. That clarity doesn't yet exist uniformly across markets.

The Liquidity Illusion

Tokenization doesn't transform the underlying economics of an asset. A 2025 academic paper examining over $25 billion in tokenized RWAs found that most tokenized assets exhibit low trading volumes, long holding periods, and limited secondary market activity. The token might be technically transferable. Finding a buyer at a fair price is a different question.

Liquidity is highest where the underlying asset already generates consistent demand - tokenized Treasuries and certain private credit pools. For more niche assets, the secondary market can be thin to nonexistent.

Custody and Attestation Risk

The token can function perfectly while the off-chain entity collapses. If custody arrangements are weak, or attestations about the underlying asset are infrequent or unverifiable, you may have no reliable way of knowing the asset behind your token exists as claimed.

Ask: Who holds the underlying asset? How often are reserves audited? By whom? What happens if the custodian fails?

Smart Contract and Oracle Risk

RWA tokens have a bigger attack surface than regular crypto. The risk doesn't stop at the smart contract - it extends into every off-chain process the token depends on: price feeds, reserve attestations, custody arrangements, and legal enforceability.

CertiK's 2025 RWA security report put it plainly: oracle manipulation, fraudulent proof-of-reserve attestations, and custodial failures are all live attack vectors. Losses from RWA-specific exploits reached $14.6 million in the first half of 2025 alone, more than double the total for all of 2024.

How to Evaluate an RWA Project

Before putting money into any RWA token or project, run through these questions:

✓ What exactly is the underlying asset? Be specific. T-bills, a loan pool, a specific building, a receivables portfolio - not just "real estate" or "private credit."

✓ Who is the issuer, and what's the legal structure? SPV, trust, fund share, or something else. If they can't explain it clearly, that's the answer.

✓ What rights does the token actually grant? Cash flows? Redemption? Governance? Collateral claim? Some tokens grant none of the above in any enforceable way.

✓ Who is the custodian, and what's their track record? Check for regulatory licensing, not just marketing claims.

✓ How does redemption work? Timing, minimums, fees, and, critically, under what conditions redemptions can be suspended.

✓ What proof exists? Audits, attestations, reserve reports, and how often they're published.

✓ What's the real liquidity? Where does it trade, what's the actual volume, and what's the spread in practice - not in theory.

✓ What smart contract controls exist? Look for independent audits, upgradeability risk, and who controls the admin keys.

RWA Is Where Blockchain Gets Serious - Keep Learning

Real world asset tokenization is not just another crypto trend to track. It is a test of whether blockchain infrastructure can do something genuinely useful beyond native digital assets, and the early results suggest it can, with caveats attached.

The market is growing fast, institutions are committed, and the asset classes coming on-chain are expanding beyond Treasuries and gold into private credit, equities, and things that have never been tradeable at this scale before.

An RWA token is only as good as the legal structure, the custodian, and the redemption mechanics behind it. Don't trust the marketing. Read the docs.

Learning Crypto gives you the tools to do exactly that. Pull live on-chain data through the Ask Crypto AI copilot, track smart money flows on the public ledger, get daily actionable market signals, and talk strategy with a private community of serious investors.

Don't trust. Verify.

Frequently Asked Questions

What is the difference between an RWA token and an NFT?

An NFT (non-fungible token) is a token standard that represents a unique, non-interchangeable asset. An RWA token can be either fungible or non-fungible, depending on the asset. A tokenized property might use a non-fungible structure; tokenized gold, by contrast, would typically be fungible. The RWA label refers to what the token represents, not to its technical structure.

How do I know a tokenized asset is backed by the real thing?

Legitimate tokenization projects publish audits, proof-of-reserve reports, or legal documentation confirming that the underlying asset exists and is held as claimed. The quality of these verifications varies significantly. Independent third-party audits by reputable firms carry more weight than issuer self-attestation.

What chains are most RWAs built on?

Ethereum dominates, largely because of its established DeFi ecosystem and institutional familiarity. Solana is growing, particularly for tokenized equities and ETFs. Stellar has a strong RWA presence too, especially for government securities.

Can I lose money on an RWA token?

Yes. The token can lose value if the underlying asset declines, if the issuer fails, if redemptions are suspended, or if secondary-market liquidity dries up. Tokenization doesn't remove investment risk. It changes the wrapper, not the underlying exposure.

Sources and Further Reading

CoinGecko RWA Report 2026 — coingecko.com/research/publications/rwa-report-2026

CertiK 2025 Skynet RWA Security Report — certik.com/resources/blog/2025-skynet-rwa-security-report

BCG + ADDX: Asset Tokenization to Reach $16 Trillion by 2030 — ledgerinsights.com/bcg-addx-estimate-asset-tokenization-to-reach-16-trillion-by-2030

Chainalysis: Tokenized RWAs and On-Chain Commodities — chainalysis.com/blog/tokenized-real-world-assets-on-chain-commodities

IOSCO: Decentralized Finance and Digital Assets Report 2024 — iosco.org

Cointelegraph: RWA Protocol Exploits Reach $14.6M in H1 2025 — cointelegraph.com/news/rwa-protocol-exploits-14-6m-in-h1-2025-surpassing-2024

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Secure your edge: Get Crypto Made Easy PDF + weekly insights—free today.

No spam, unsubscribe at any time. By subscribing, you agree to our Privacy Policy. Need to unsubscribe? Unsubscribe from newsletter.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Cryptocurrency investments carry risk; you should always do your own research before making any investment decisions.

Heidi Chakos is co-founder of LearningCrypto and creator of the @cryptotips YouTube channel. A cryptocurrency educator and author with over a decade in the space, she specialises in Bitcoin fundamentals, self-custody, and on-chain analytics. Follow her on X at @blockchainchick.

View all articles →