What Is KYC in Crypto? Know Your Customer Explained

by Heidi Chakos

by Heidi ChakosTL;DR KYC (Know Your Customer) verifies your identity before you access certain crypto services, such as centralized exchanges or fiat onramps. It helps platforms comply with regulations, prevent fraud, and maintain banking relationships, but it also introduces privacy trade-offs.

When you sign up for your first crypto exchange, you're asked to upload your driver's license, take a selfie, and prove where you live. If you've been around crypto for any length of time, you know this drill: it's called KYC, or "Know Your Customer."

For newcomers, this feels backward. Isn't crypto supposed to be permissionless? Wasn't the whole point to escape banks and identity checks? Yes, but only in parts of the crypto world. Anywhere crypto touches traditional money, KYC shows up. The question isn't whether KYC exists, but where you'll run into it and whether you can work around it.

Some crypto services demand full identity verification. Others don't ask for anything. The difference comes down to what you're doing and who you're doing it with. Once you know where the boundaries are, you can pick platforms that match what matters to you, be it convenience, privacy, or something in between.

What You'll Learn in This Guide

➤ What KYC means in crypto. The term comes from banking, but it works differently when applied to decentralized technology.

➤ Why exchanges require identity checks. Regulatory pressure is part of it, but there are other reasons platforms ask for your information.

➤ How the verification process actually works. From document uploads to selfie checks, here's what happens when you complete KYC.

➤ What information gets collected. Name and address are obvious, but platforms track more than you might expect.

➤ The real trade-offs. KYC offers protection and access, but it comes with privacy costs that matter to many users.

➤ How KYC differs from AML. These terms get used interchangeably, but they're not the same thing.

➤ Where you need KYC and where you don't. Centralized exchanges require it. Self-custody wallets don't. The line is clearer than you think.

What Does KYC Mean in Crypto?

KYC stands for "Know Your Customer." The process exists to verify identity, and while that sounds straightforward, the reasons behind it get more complicated when you're dealing with a technology designed to work without middlemen.

Traditional banks have used KYC for decades. Crypto platforms borrowed the framework, but applied it selectively. Not every part of crypto requires it.

KYC Explained Simply

At its core, KYC is an identity check. The term "Know Your Customer" comes from banking regulations that require financial institutions to verify who they're doing business with. Banks need to confirm you are who you claim to be, primarily to prevent money laundering and fraud.

Crypto platforms adapted this framework when they started connecting cryptocurrency to traditional money. If an exchange lets you buy Bitcoin with a credit card or withdraw funds to your bank account, they need to follow the same rules banks do.

That means collecting your personal information and checking it against government databases.

KYC acts as a gatekeeper. Pass the verification, and you get access to services like fiat deposits, higher withdrawal limits, and certain trading features. Fail it or skip it, and you're locked out of those services entirely.

Why Crypto Platforms Use KYC

Regulatory pressure is the biggest driver. In most countries, any business that handles fiat currency must comply with financial regulations. That includes anti-money laundering laws, which require platforms to identify their users.

Regulators don't care whether you're a traditional bank or a crypto exchange. If you're converting dollars to Bitcoin, you're in their jurisdiction.

Fiat onramps depend on banking relationships. Exchanges need bank accounts to accept deposits and process withdrawals. Banks won't work with crypto platforms unless those platforms follow KYC rules.

Without banking access, an exchange can't offer the one thing most new users want: a way to buy crypto with a debit card.

Fraud prevention. Anonymous accounts are easier to use for scams, stolen funds, and account takeovers. KYC doesn't eliminate fraud, but it adds friction that makes certain attacks harder to pull off at scale.

Licensing requirements vary by country, but most jurisdictions require crypto businesses to register as money services or financial institutions. Those licenses come with mandatory KYC obligations.

Platforms that want to operate legally across multiple countries often implement KYC to meet the strictest regulations they face.

How KYC Works in Crypto Platforms

The KYC process isn't complicated, but it takes time. Each platform handles verification slightly differently, but the basic steps are consistent across major exchanges. You'll submit documents, wait for approval, and sometimes deal with requests for additional information if something doesn't match up.

The process exists to create a verified identity trail that links your real-world identity to your crypto account. Once you're in the system, that verification doesn't just disappear. Platforms continue monitoring account activity and may ask you to reverify periodically.

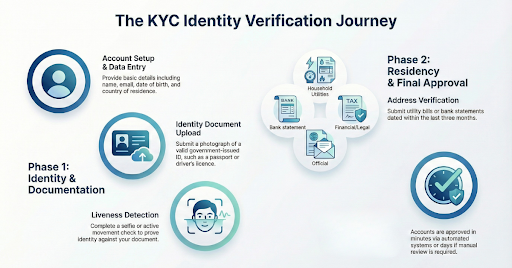

Typical KYC Verification Steps

The verification process follows a predictable sequence:

Account creation: Enter basic information - name, email, phone number, date of birth, and country of residence. Some platforms let you browse without verification, but you can't deposit funds or trade until you complete the full process.

Identity document upload: Submit a government-issued ID, such as a passport, driver's license, or national identity card. You'll photograph both sides of the document while their system checks whether the information matches what you entered during signup.

Selfie or liveness check: Prove you're the person in the ID photo. Basic verification asks for a selfie holding your ID. More advanced systems use liveness detection, where you'll turn your head, blink, or follow on-screen prompts to prove you're not using a photo of someone else.

Address verification - Submit proof that you live where you claim to live. Accepted documents include:

Utility bills (electric, water, gas)

Bank statements

Government correspondence

Tax documents

The document needs to show your full name and current address, dated within the last three months.

Approval timeline - Wait for verification. Automated systems can approve accounts in minutes if everything matches cleanly. Manual review kicks in when something looks off, which can take hours or days.

What Information Is Collected

Personal Details | Full legal name, date of birth, nationality, residential address, phone number, and sometimes employment information or source of funds |

Government ID | Image files of your ID, extracted data like ID number, issue date, expiration date, and biometric data from facial recognition scans |

Proof of Address | Copies of utility bills or bank statements, which means they now have information about your other financial accounts |

Device & IP Data | Login locations, device fingerprints, and browser information are collected automatically every time you access your account |

Ongoing Monitoring

KYC isn't a one-time checkpoint. Platforms continue watching account activity after you're verified:

Transaction monitoring flags unusual patterns like large deposits, rapid trading, or transfers to high-risk addresses. If the system detects something it doesn't like, your account might get frozen until you explain what you're doing.

Periodic reverification happens when your ID expires or when a platform updates its compliance requirements. You'll get a notification asking you to resubmit documents, and your account features might be limited until you comply.

Account restrictions can appear without warning. If your activity triggers certain thresholds or if regulations change in your country, the platform might reduce your withdrawal limits, disable fiat deposits, or require additional documentation before you can access your funds again.

KYC vs AML in Crypto

KYC checks who you are. AML watches what you do. Both serve compliance, but at different moments.

KYC is the bouncer at the door. AML is the security camera inside. You deal with one to get in, and the other watches you the whole time you're there.

What Is AML?

AML stands for Anti-Money Laundering. Platforms use it to catch financial crimes in real time.

KYC asks for your passport. AML asks why you just moved $50,000 through three different wallets at 2 am on a Tuesday.

The regulations behind both come from the same place, but AML cares about patterns, not documents. If your account starts behaving like a money laundering operation, the system flags it. Sometimes that means a frozen account. Sometimes it means the platform reports you to authorities without telling you first.

Differences Between KYC and AML

KYC | AML |

Verifies identity | Monitors behavior |

Happens at account creation | Happens continuously |

One-time process (with periodic updates) | Ongoing surveillance |

Collects documents and personal data | Analyzes transaction patterns |

Answers "who is this person?" | Answers "what are they doing?" |

KYC gives the platform your identity. AML watches whether that identity does anything suspicious.

You can't have effective AML without KYC. You verify once. They watch forever.

Where Is KYC Required in Crypto?

Not every crypto service demands your ID. If you're moving money between crypto and fiat, expect KYC. If you're staying entirely on-chain, you can often avoid it completely.

Decentralized protocols that run on smart contracts don't have anyone to enforce KYC, even if they wanted to.

Centralized Exchanges

Major exchanges like Kraken, Coinbase, and Binance require full KYC verification for most features. You might be able to create an account and browse markets without it, but you can't do much else.

Fiat trading is the main trigger. The moment you want to deposit dollars, euros, or any government currency, KYC becomes mandatory. Banks won't process transactions for exchanges that don't verify users, which means exchanges can't offer fiat pairs without implementing verification.

Withdrawals often have KYC gates too. Some platforms let you deposit crypto without verification, but they won't let you withdraw it until you complete KYC. Others impose strict limits on unverified accounts, making them essentially useless for anything beyond testing.

Fiat Onramps and Offramps

Anywhere crypto meets traditional money, KYC appears. These services exist specifically to bridge the gap between the two systems, which means they operate under the strictest rules.

Buying crypto with bank cards requires verification on every platform that offers it. Whether you're using a dedicated onramp service like MoonPay or buying directly through an exchange, you'll submit documents before your first purchase goes through. Credit card companies and banks demand it.

Selling crypto for fiat works the same way. You can't cash out to your bank account without proving who you are. The platform needs to verify that the bank account belongs to you, which means KYC documentation ties your identity to both sides of the transaction.

Where KYC Is Usually Not Required

With decentralized crypto infrastructure, nobody's checking IDs. These tools work without intermediaries, which means there's no central authority enforcing verification requirements.

Self-custody wallets like MetaMask, Trust Wallet, or hardware wallets never ask for identification. You download the software or buy the device, generate a wallet, and you're done. No company controls your keys, so no company can demand your documents.

Decentralized exchanges operate peer-to-peer through smart contracts:

Uniswap

PancakeSwap

dYdX

SushiSwap

You connect your wallet, swap tokens, and disconnect. The protocol doesn't know your name and doesn't care. All it sees is a wallet address executing trades.

On-chain protocols for lending, staking, or yield farming operate the same way. You interact with smart contracts, not companies. DeFi platforms don't have compliance departments because there's no company to comply with. The code runs permissionlessly.

Pros and Cons of KYC in Crypto

KYC isn't inherently good or bad. It depends on what you're trying to do and what you're willing to give up.

Some users prioritize access to regulated services and don't mind sharing documents. Others view any identity verification as a dealbreaker. Both perspectives can make sense.

Advantages of KYC

Benefit | Why It Matters |

✓ Consumer protection | Verified accounts have recourse when something goes wrong. If your account gets hacked or the platform makes an error, you can work with support to recover funds. Anonymous accounts get no help. |

✓ Recovery options | Forgot your password? Lose your 2FA device? KYC-verified accounts can reset access through identity verification. Without it, you're locked out permanently. |

✓ Regulatory access | KYC platforms can offer services that non-KYC platforms can't, like fiat deposits, credit card purchases, higher withdrawal limits, and access to certain tokens that regulators classify as securities. |

✓ Reduced fraud | Identity verification makes it harder to create fake accounts, run scams, or use stolen payment methods. It doesn't eliminate fraud, but it raises the barrier. |

Drawbacks and Privacy Concerns

Risk | What It Means |

✗ Data breaches | Crypto exchanges get hacked. When they do, KYC databases leak. Your passport, address, and selfie end up on dark web marketplaces where criminals use them for identity theft. |

✗ Loss of anonymity | Once you verify on a platform, your crypto activity gets tied to your real identity. Governments, hackers, and anyone who accesses the database can see what you trade and when. |

✗ Surveillance concerns | KYC creates permanent records of your financial activity. Regulators can request this data, and platforms must comply. What's legal today might not be tomorrow. |

✗ Exclusion risks | KYC requirements lock out people without government IDs, people in unsupported countries, and anyone who can't pass automated verification. Financial access becomes conditional. |

Is KYC Against the Spirit of Crypto?

Depends on who you ask and what part of crypto they care about.

Original Cypherpunk Ideals

The cypherpunks who built the foundation for Bitcoin wanted financial systems that worked without asking permission. No banks. No governments. No proving who you are to access your own money.

Satoshi designed Bitcoin so anyone could download the software and use it without identifying themselves. That was the whole point.

KYC contradicts that vision completely. Uploading your passport to trade crypto is exactly what early adopters were trying to escape. If the goal was censorship-resistant money, requiring government identification to access it defeats the purpose.

Permissionless Systems vs Regulated Gateways

Here's the practical problem: most people want to use crypto with fiat money. They want to buy Bitcoin with their debit card, trade it on an exchange with customer support, and cash out to their bank account when they're done.

Those bridges between crypto and traditional finance can't exist without regulation. Banks won't touch crypto companies that ignore KYC rules.

The Practicalities of Mass Adoption

Crypto split into two worlds. One stays true to the cypherpunk vision with self-custody wallets, decentralized exchanges, and purely on-chain activity. The other compromises on ideology to gain mainstream access through regulated platforms that implement KYC.

Want to use Bitcoin the way Satoshi intended? You still can. Generate a wallet, buy peer-to-peer, trade on DEXs, never upload an ID. That option never disappeared.

Want to buy crypto with Apple Pay and call customer service when something breaks? That's available too. Just costs your privacy.

The cypherpunk dream didn't die. It just stopped being the only option. The rails still run permissionlessly. The onramps charge admission.

Should You Use KYC or Non-KYC Crypto Services?

There's no rulebook here. It’s ultimately your choice. Satoshi isn't looking down from some blockchain in the sky, judging your choices.

Most people end up using both. They onboard through KYC exchanges for convenience, then move funds to self-custody wallets for long-term storage, and trade on DEXs.

Now you know where you stand on KYC, the next challenge is actually using crypto effectively.

Learning Crypto cuts through the noise with real-time blockchain insights, smart-money wallet tracking, and AI assistants that answer your questions using live on-chain data. Over 5,000 users already skip the trial-and-error.

Frequently Asked Questions

Is KYC mandatory for all crypto users?

No. KYC only applies when you use centralized platforms that connect to traditional banking systems. If you stick to self-custody wallets, decentralized exchanges, and on-chain protocols, you can use crypto without ever verifying your identity.

Can you buy crypto without KYC?

Yes, but your options are more limited. You can buy crypto peer-to-peer, use Bitcoin ATMs that don't require verification for small amounts, or earn crypto directly through mining or providing services.

Is crypto KYC safe?

It depends on the platform's security practices. KYC databases contain sensitive personal information that becomes valuable to hackers. Several major exchanges have suffered data breaches that exposed user documents. The process itself is as safe as the company storing your data.

Can KYC data be misused?

Unfortunately, yes. Once you submit documents to an exchange, you lose control over how that data gets used or stored. Exchanges can share your information with government agencies, third-party verification services, or law enforcement without notifying you. If the exchange gets hacked or goes bankrupt, your documents could end up in the wrong hands. There's also a risk that employees will misuse access to customer data.

What happens if I fail KYC verification?

Your account gets restricted or closed. Some platforms let you withdraw existing crypto but prevent new deposits or trades. Others freeze your account entirely until you resolve the verification issue. You can usually resubmit documents, but repeated failures might result in permanent account closure.

Can I use the same KYC for multiple exchanges?

No. Each platform runs its own verification process. You need to complete KYC separately for every centralized exchange you use. There's no universal crypto passport that transfers between platforms.

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Secure your edge: Get Crypto Made Easy PDF + weekly insights—free today.

No spam, unsubscribe at any time. By subscribing, you agree to our Privacy Policy. Need to unsubscribe? Unsubscribe from newsletter.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Cryptocurrency investments carry risk; you should always do your own research before making any investment decisions.

Heidi Chakos is co-founder of LearningCrypto and creator of the @cryptotips YouTube channel. A cryptocurrency educator and author with over a decade in the space, she specialises in Bitcoin fundamentals, self-custody, and on-chain analytics. Follow her on X at @blockchainchick.

View all articles →