Tokenomics Explained: Master Crypto Project Economies & Value

by Heidi Chakos

by Heidi ChakosTokenomics is the economic design of a crypto project. It governs how tokens are created, distributed, and managed, and it largely decides whether a project has staying power or just a price chart. Get tokenomics right, and a project can compound value over years. Get it wrong, and the supply quietly devours the price. |

Plenty of traders get into crypto by watching charts. They see something pump, read a few hyped-up tweets, and start hunting for an entry. What they almost never do is look at what sits underneath the price.

That underneath has a name. Tokenomics.

Skip it, and you're buying a business without checking the books. The shop might look busy. Doesn't mean the numbers work.

What follows is a proper breakdown. What tokenomics is. How the moving parts fit together. What good design actually looks like today, after a few cycles of market lessons. And how to run a real analysis on any project before you commit serious time or money to it.

What You'll Learn

What tokenomics actually means and why it separates sustainable crypto economies from elaborate countdowns to collapse

How supply mechanics shape value so you can read a token's circulating supply, total supply, and unlock schedule for what they really say

What real utility looks like versus utility theatre dressed up to justify a token launch

Why tokenomics designs fail and the structural patterns that have wrecked projects

A practical analysis framework with the metrics, ratios, and red flags that consistently matter

What Is Tokenomics? The Economic Engine of Crypto Projects

The word mashes "token" and "economics" together, but that sells it short. Tokenomics is the full economic design of a crypto project. The rules for how a token gets created, allocated, distributed, and used inside its ecosystem.

Think constitutional rules for a small economy. Who gets wealth at the start. How new wealth is created. What gives the currency value. What happens when people try to game the system.

Bad rules don't just produce bad outcomes. They produce predictable bad outcomes. Sometimes slowly. Sometimes overnight.

What makes tokenomics so easy to overlook is that most of it is hardcoded at launch. A central bank can adjust rates and pump the brakes. Most crypto projects can't. The rules are written into smart contracts and visible on-chain before you ever buy in.

So the information is there. Hardly anyone bothers to look.

Tokenomics isn't price commentary. It's the blueprint for the entire project economy.

Reading it tells you whether a project rewards genuine participation or quietly transfers value from late buyers to early insiders. Two very different machines. They don't always look different from the outside.

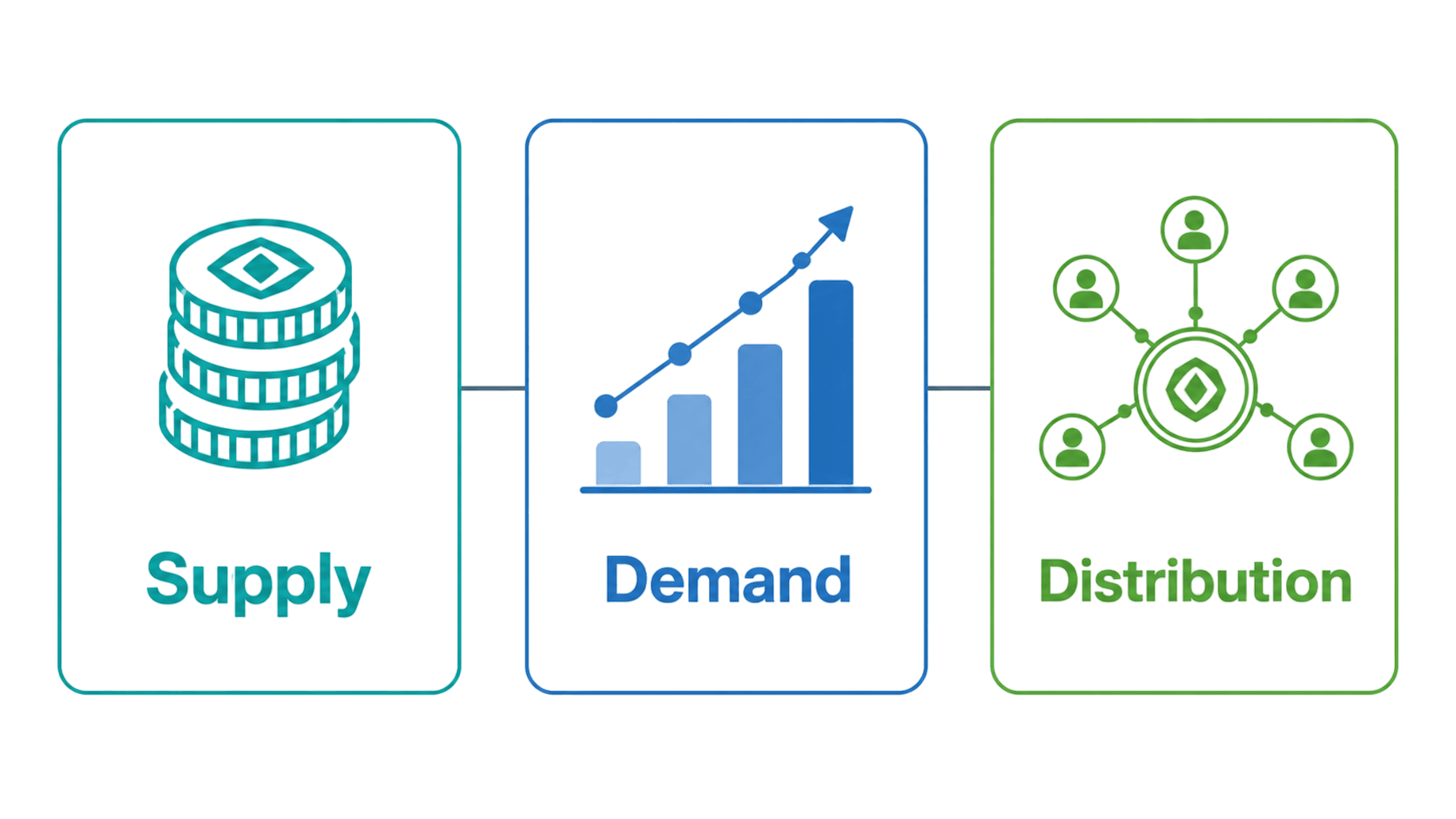

The Three Pillars of Tokenomics: Supply, Demand, and Distribution

Every tokenomics model rests on three things. How much of the token exists How does it get into people's hands. And what creates real demand for it.

Each shapes the others. Compounded over months and years, small differences in design produce wildly different outcomes.

Token Supply & Scarcity: Understanding Limits and Inflation

Supply is the most visible lever, and it shows up in a few forms.

Total supply is the maximum number of tokens that will ever exist.

Circulating supply is what's actually in the market right now.

The gap between those two numbers is one of the most under-read figures in crypto. A token trading cheaply with most of its supply still locked carries a very different risk profile than its market cap suggests.

Inflation mechanics control how fast new tokens enter circulation. Bitcoin's hard cap of 21 million coins and four-yearly halving schedule create predictable scarcity by design. Other projects run inflationary models that keep issuing tokens to reward validators or stakers.

Neither approach is automatically better. Heavy inflation in a token with thin demand is a slow bleed dressed up as a yield strategy.

Deflation can be engineered too, usually through burns that permanently remove tokens from supply. We'll get to those.

The principle: high demand against fixed or shrinking supply tends to lift value. High inflation against flat demand does the opposite, no matter how clever the marketing.

Distribution Models: How Tokens Get Into Users' Hands

How a token is initially distributed shapes the power dynamics of the whole ecosystem. The common mechanisms:

ICOs and IDOs - tokens sold to the public ahead of, or at, launch

Airdrops - free distributions to wallets that meet certain criteria

Mining and staking rewards - tokens issued for securing the network

Direct allocations - to teams, investors, treasuries, and ecosystem funds

Always ask the same question. Who benefits first, and at whose cost?

Early investors and founding teams get tokens at deep discounts. That's not automatically corrupt. Early risk deserves reward.

What matters is the size of the allocation and the schedule for releasing it. A project where insiders hold 40% of supply with no lockup is a different beast from one where team tokens vest over four years with a 12-month cliff.

Airdrops deserve their own paragraph.

Done well, distributed to genuine users based on real on-chain activity, they bootstrap decentralization. Done badly, they attract mercenary farmers who dump the moment tokens land.

Berachain's BERA airdrop in February 2025 became the textbook example. The token pumped 71% in hours, then crashed 63% as airdropped supply hit the market.

Demand Drivers: What Makes a Token Valuable?

Supply mechanics create scarcity. Demand mechanics create the reason anyone wants the token in the first place.

Speculative demand is fragile. People buy because they think someone else will pay more later. Works until it doesn't.

Durable demand comes from utility. The token is needed to access a service. To vote on governance. To earn yield. To pay fees inside an ecosystem that people actually use.

When a token is genuinely load-bearing, the demand signal looks completely different from one that's just a vehicle for speculation.

Utility & Value Accrual

Tokens that hold value over time and tokens that don't usually split on a single question. Does this token actually do anything?

Utility is how value accrues to holders. It's also where most projects fall short. Launching a token is easy. Designing real reasons to hold one is hard.

Governance Tokens: Giving Power to the Community

Governance tokens give holders voting rights on protocol decisions. Fee structures. Treasury allocations. Major upgrades. The theory is clean. The people most invested get a real say in how things evolve.

Practice is messier. Governance participation in most DeFi protocols is low. Whales call the shots.

But where voting power is broadly distributed, and there are decisions worth voting on, governance tokens build genuine community ownership. The token becomes a stake in the project's future, not just a trading instrument.

Staking & Yield Generation: Earning Rewards With Your Tokens

Staking locks tokens into a protocol in exchange for rewards. For proof-of-stake networks, this does real work. Validators put up collateral that gets slashed if they misbehave. The network gets security. Fair trade.

The critical question is what funds the rewards.

Real protocol revenue from real users? Or pure token inflation?

The second one is what some analysts call yield laundering. Returns that look like income but are really just diluting your share of supply. A staking model is only as solid as the economic activity behind it.

Burning Mechanisms: Deflationary Pressure and Value

Token burning permanently removes tokens from circulation.

Ethereum's EIP-1559 upgrade, launched in August 2021, sends a portion of every transaction's base fee to a burn address instead of paying it to validators. Around 4.6 million ETH burned to date.

There's a wrinkle in 2026. After the Dencun upgrade in March 2024 moved most Layer-2 activity off mainnet, base fee revenue collapsed. ETH has been mildly inflationary at around 0.23% per year through 2025 and into 2026. The "ultrasound money" thesis isn't dead. It's just contingent on mainnet activity holding up.

The lesson generalizes. Burn mechanisms only matter if the burning is substantial against issuance. A project minting 10 million tokens a month and burning 50,000 has a deflationary story on paper and an inflationary reality on-chain.

Always look at net issuance.

Access & Utility Tokens: Unlocking Platform Features

Some tokens function as keys. You need them to access features, pay for services, or do specific things on a platform. When the platform has real users, you get consistent buy pressure.

When it has no usage, the token is a key to an empty room.

The honest question is whether the token is genuinely required, or whether it's friction the project added to invent a use case. The first creates durable value. The second gets engineered away the moment users have a better option.

How to Analyze a Project's Tokenomics: A Practical Framework

Key Metrics to Monitor

Market cap vs. fully diluted valuation (FDV). Market cap is the price times what's circulating now. FDV is the price times every token that will ever exist. A project with a modest market cap and an enormous FDV is signaling a wave of supply unlocks ahead. Future sellers, all queued up.

The 2024 to 2026 period made this brutally clear. Low-float, high-FDV launches became the standard playbook.

At the Ethereum Community Conference (EthCC) in early 2026, 21Shares researchers were calling token failure rates the highest on record. The market cap-to-FDV ratio is now one of the first numbers that experienced traders check.

Circulating supply percentage. What fraction of total supply is actually circulating? A low percentage combined with aggressive inflation or upcoming unlocks creates predictable downward pressure.

Vesting and unlock schedules. When do team and investor tokens hit the market? Tools like TokenUnlocks and CryptoRank track upcoming unlocks. A 10% supply unlock heading into a quiet market is a known sell pressure event.

Holder concentration. Etherscan, Arkham, Bubblemaps, and Nansen will show you the top-ten holders of any token in seconds. If three addresses control 60% of supply, that's a meaningful data point.

Revenue vs. incentive spend. Does the protocol generate real fee revenue? How does that compare to what it spends on liquidity mining or staking rewards? A project spending 10x its revenue on incentives is borrowing time. DefiLlama and Token Terminal publish this data for major protocols.

Red Flags

Some patterns reliably indicate problems:

A big slice of supply allocated to the team with minimal lockup

Anonymous teams with no accountability and large treasury control

APY rewards nobody can explain in terms of revenue

Vague or missing documentation on token distribution

Governance that's nominally decentralized, but where one entity retains veto power

Low float, high FDV launches with vesting cliffs expiring into thin liquidity

One of these doesn't disqualify a project. Several together is a different conversation. Look for clusters, not single items.

Transparency Is the Floor

Token allocations, vesting schedules, emission curves, treasury holdings. All of it should be publicly documented and verifiable on-chain. If a project asks you to take its tokenomics on trust, that's already telling you something.

Economic audits are different from technical ones. A clean technical audit tells you the contracts do what the documentation says. An economic audit tells you whether what they say they do actually makes sense. Worth looking for.

Discover our Complete DYOR Research Framework Here

Case Studies: Good vs. Bad Tokenomics

The clearest way to learn tokenomics is to look at what's held up over time and what's blown up in public.

Tokenomics That Worked

Bitcoin. Still the cleanest design in crypto. 21 million hard cap. Halving every four years. No team allocation, no investor cliffs, no governance keys.

The whole monetary policy is visible in the code and effectively immutable. Every halving since 2012 has compressed new issuance further. That's why Bitcoin is called digital gold rather than just another crypto.

Hyperliquid (HYPE). The standout fair-launch story of 2024. The on-chain perpetuals exchange airdropped 31% of supply directly to over 90,000 active users in November 2024. No VC allocation. Team tokens locked for at least a year.

What makes the design durable is the buyback. Hyperliquid uses real protocol revenue to buy HYPE off the market every day. By August 2025, monthly trading fees on the platform exceeded $100 million, all of it cycling back into buybacks. Demand for the platform translates directly into demand for the token.

Aave (AAVE). A traditional DeFi example worth studying. Aave is the largest decentralized lending protocol with over $36 billion TVL by late 2025 and annualized fees past $350 million. In April 2025, the DAO began using $1 million per week in revenue to buy AAVE off the market. By November, the buyback was made permanent.

Real fees funding buy pressure rather than emissions diluting it. Not perfect, but structurally right.

The pattern across all three: revenue or scarcity that's load-bearing, not cosmetic.

Tokenomics That Failed

Iron Finance (TITAN), June 2021. Partial-collateral algorithmic stablecoin. TITAN ran from a few cents to nearly $65 in weeks. Then large holders started selling, and the rebalancing mechanism turned into a death spiral. TITAN went from $64 to fractions of a cent in hours. Mark Cuban famously got caught in it.

Lesson: tokenomics that depend on perpetually rising demand aren't tokenomics. They're momentum dressed up as design.

Terra (UST and LUNA), May 2022. The biggest tokenomics failure in crypto history. UST was an algorithmic stablecoin backed by minting and burning LUNA. Anchor Protocol offered roughly 20% yield on UST deposits, funded by Terra's treasury rather than real revenue.

When confidence cracked, LUNA's supply ballooned from 350 million tokens to over 6.5 trillion in days as the protocol tried to defend the peg. Both tokens went effectively to zero. Around $40 billion erased.

The Anchor yield was the warning sign in plain sight.

Low-float, high-FDV launches, 2024 to 2026. Less a single project than an entire era. Aptos, Sui, StarkNet, Worldcoin, and dozens of others launched with under 20% of supply circulating, propped up at FDVs of several billion dollars.

Locked team and investor tokens then unlocked into thin liquidity over the following year or two. Berachain's BERA in February 2025 was one of the most public examples. 71% pump on launch, 63% crash inside the same week.

By early 2026, token failure rates were at record highs, and the low-float / high-FDV model was widely identified as the structural cause.

The throughline across all the failures is the same. Returns not backed by something real. Supply that overwhelms demand. Insiders winning at retail's expense.

The failure modes don't change much. Just the wrapping paper.

Tokenomics Knowledge Is a Long-Term Edge

Most of the failed tokenomics in this article share one thing. The information was on-chain the whole time. People just didn't know what to look for, or didn't have the tools to check it fast enough.

That's the gap Learning Crypto fills. The Ask Crypto AI Copilot lets you interrogate any project's on-chain data in seconds. The Daily On-Chain Brief tells you what actually moved this week without the influencer spin. The community is full of people who learned the hard way that "trust me bro" isn't a strategy.

Step outside the system. Verify the truth yourself.

Frequently Asked Questions

What is tokenomics in simple terms?

The economic rules of a crypto project. How tokens are created, distributed, and used. It covers supply limits, inflation rates, who holds what, and what the token does inside its ecosystem.

Why does tokenomics matter for crypto investors?

Because price tells you almost nothing about long-term value. A token can look cheap while sitting on a mountain of unreleased supply that will dilute holders for years. Tokenomics shows the structural incentives underneath.

What is the difference between market cap and fully diluted valuation?

Market cap is the current price times circulating supply. FDV applies that price to every token that will ever exist. A large gap between the two signals significant future supply hitting the market.

What makes a token deflationary?

When the rate at which it's removed from supply, usually through burning, exceeds the rate new tokens are created. Ethereum was deflationary during periods of heavy mainnet activity after EIP-1559. After the Dencun upgrade in 2024 shifted activity to Layer 2s, ETH has been mildly inflationary at around 0.23% annually.

How do vesting schedules protect token holders?

They delay when team members and early investors can sell their allocations, usually over one to four years. Cliff periods add extra delay before any tokens release at all, typically 6 to 12 months. The point is to align insider incentives with long-term project success.

Can tokenomics change after a project launches?

Sometimes. Projects with active governance can vote to change emission rates, burn mechanisms, or treasury allocations. Hardcoded limits like Bitcoin's 21 million cap are effectively immutable. Always check what's fixed and what's adjustable.

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Secure your edge: Get Crypto Made Easy PDF + weekly insights—free today.

No spam, unsubscribe at any time. By subscribing, you agree to our Privacy Policy. Need to unsubscribe? Unsubscribe from newsletter.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Cryptocurrency investments carry risk; you should always do your own research before making any investment decisions.

Heidi Chakos is co-founder of LearningCrypto and creator of the @cryptotips YouTube channel. A cryptocurrency educator and author with over a decade in the space, she specialises in Bitcoin fundamentals, self-custody, and on-chain analytics. Follow her on X at @blockchainchick.

View all articles →