CBDCs vs Cryptocurrency: Central Control vs Financial Freedom

by Heidi Chakos

by Heidi ChakosCBDCs (Central Bank Digital Currencies) are government-issued digital money controlled by central banks. Cryptocurrencies are decentralized, permissionless, and censorship-resistant. They're both digital, but philosophically opposite. CBDCs give the state a direct line to every transaction you make. Crypto was built to prevent exactly that. |

Governments keep saying they're building "digital money." So does crypto. And because both live on screens instead of in your pocket, it might be assumed they're basically the same thing.

They're not. Not even close.

CBDCs are digital cash designed by central banks, for central banks. Every transaction logged. Every balance visible. Every rule set by the state. Cryptocurrency was built to do the opposite. No central authority. No permission needed. No off switch.

The fact that both get called "digital money" is the biggest misdirection in finance right now.

One gives you a new way to pay. The other gives governments a new way to watch.

What You'll Learn about CBDCs and Crypto

→ What a CBDC actually is and why it's nothing like the money in your bank app

→ The global scoreboard: who's building them, who's banned them, and who's gone full send

→ Programmable money, frozen accounts, and total surveillance: the things central banks don't lead with

→ CBDCs vs crypto side by side: same screen, completely different philosophies

→ Why CBDCs actually strengthen the case for crypto, not weaken it

What Is a CBDC?

A CBDC is a digital version of a country's currency, issued and controlled directly by its central bank. Not a cryptocurrency. Not a stablecoin. And not the balance sitting in your banking app right now.

That balance? It's your bank's IOU. Your bank owes you that money, and you trust them to cough it up when you ask. A CBDC skips that relationship entirely. It's a direct claim on the central bank itself. Government-issued digital cash that lives in a wallet on your phone. Sounds convenient. Except unlike actual cash, the government can see every single thing you do with it.

We're going to assume you already know what cryptocurrency is. If you're still getting your head around that side of things, check out our resources section first. This article only makes sense if you understand what crypto is trying to do.

Retail vs Wholesale

There’s two types of CBDC.

Retail CBDCs are for everyday people. Buying groceries, paying rent, sending money to your mate.

Wholesale CBDCs are for banks and financial institutions settling big transactions between themselves. Most of the privacy concerns sit squarely on the retail side. For obvious reasons.

How CBDCs Work

A CBDC runs on a centralized or hybrid ledger operated by the central bank. Some borrow distributed ledger tech. Some don't bother. But even the ones that pinch ideas from blockchain architecture keep full control with the issuing authority.

The central bank writes the rules, validates transactions, and owns the ledger. They get to decide who can hold it, how much they can hold, and what conditions come attached to spending it.

So yes. Digital money. But the "who's running the show" part is doing all the heavy lifting.

How Did We Get Here?

Central banks had been poking at the idea of digital currency since the late 1990s. Mostly in academic papers nobody read.

China's People's Bank started proper research in 2014. Sweden's Riksbank kicked off the e-krona project in 2017 because physical cash use was falling off a cliff, and they feared losing public access to central bank money entirely. The Bank of England was scribbling away on it around the same time.

Then Facebook announced Libra in 2019, and the whole thing went from back-burner research to full-blown arms race. A private company with 2 billion users building its own global currency?

Central banks that had been taking their sweet time suddenly found budgets, deadlines, and a reason to care.

Where CBDCs Stand Right Now

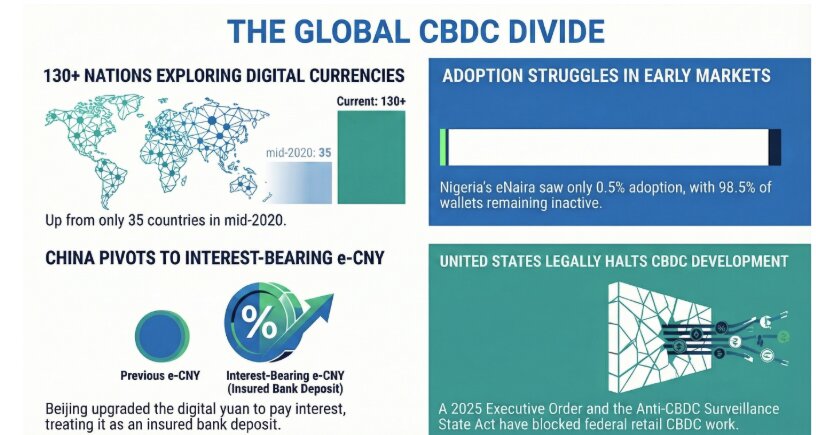

Over 130 countries are exploring CBDCs. That number was 35 in mid-2020. But "exploring" covers everything from vague research papers to fully operational systems. The actual picture is messier and more interesting than the headline suggests.

The Early Movers

Three countries have fully launched a retail CBDC: the Bahamas, Jamaica, and Nigeria.

The Bahamas rolled out the Sand Dollar in October 2020, making it the world's first. It was built for a genuine problem. Hundreds of islands, a thin banking infrastructure, and hurricanes that regularly knock out financial services. Fair enough.

But circulation has stayed stubbornly low, sitting under 1% of total Bahamian dollars in circulation years after launch.

Jamaica's JAM-DEX is operational and integrated into the national payment system. Quiet. Functional. Not making headlines.

Nigeria's eNaira is the cautionary tale. Launched in October 2021, first in Africa, with big ambitions. The reality? Only 0.5% of Nigerians adopted it. 98.5% of wallets sat inactive. The app was pulled from Google Play.

The government offered 5% discounts on taxi rides to get people to try it. Didn't move the needle. Nigeria is now exploring a separate stablecoin initiative instead, which tells you everything you need to know about how the eNaira went.

The Big Pushers

China is the one everyone watches. The digital yuan (e-CNY) has processed 3.48 billion cumulative transactions worth around $2.37 trillion.

And in January 2026, Beijing did something no other country has tried. They upgraded the e-CNY from a cash-like instrument to an interest-bearing digital deposit money. Banks now pay interest on your digital yuan balance. It's covered by deposit insurance. 22 banks are onboarded.

China essentially stopped calling it a CBDC and started treating it as a new type of bank account, one that the state still controls completely.

India's e-Rupee has seen circulation jump fourfold in a year, from ₹234 crore to over ₹1,016 crore by March 2025. Sounds impressive until you realize it still represents just 0.006% of banknotes in circulation. Six million users across 17 banks. The RBI is testing programmable payments for government transfers and exploring cross-border pilots, but daily adoption remains tiny next to UPI, which already handles 20 billion transactions a month.

The EU's Digital Euro is heading for legislation in 2026, with pilots potentially starting in 2027. The ECB has already said it won't pay interest on digital euro holdings and will cap how much you can hold. They're deliberately making it unattractive as a savings tool.

Brazil is integrating its DREX (Digital Real) with the Pix payment system for wholesale and programmable transactions.

The US Says No to CBDCs

Then there's the United States. Going the other direction entirely.

In January 2025, President Trump signed an executive order halting all federal work on a retail CBDC.

The Anti-CBDC Surveillance State Act (H.R. 1919) passed the House 219-210 in July 2025. The Senate companion bill is still in committee. But anti-CBDC provisions were also bolted onto a housing bill that passed the Senate 89-10 in March 2026.

Several states, including North Carolina and Louisiana, have passed their own bans.

The US isn't just ignoring CBDCs. It's actively legislating against them while simultaneously promoting private stablecoins through the GENIUS Act. The message is clear: digital dollars, yes. Government-controlled digital dollars, no.

Worth remembering that political winds shift fast. A new administration could reverse the executive order overnight.

Why CBDCs Should Make You Uncomfortable

Governments don't build new financial infrastructure because they want to make your life easier. If that was the goal, they'd have fixed bank transfer speeds twenty years ago.

CBDCs get sold on convenience, inclusion, and efficiency. And those aren't lies exactly. But they're the brochure. The terms and conditions tell a different story.

Every Transaction, Recorded

Cash is anonymous. You hand someone a note, they hand you a coffee. Nobody in government knows it happened. That's not a bug. That's a feature of physical money that has existed for thousands of years.

CBDCs delete that entirely. Every payment you make gets logged on a ledger the central bank can access. Your morning coffee, your political donations, your medical bills, what you bought that you'd rather not talk about. All visible. All stored.

And this isn't a worst-case scenario reading of the fine print. The Bahamas' Sand Dollar website openly states it provides a "fully auditable transaction trail" that is "non-anonymous." They're not hiding it. They're listing it as a feature.

Money With Conditions Attached

This is the part that should really keep you up at night. CBDCs can be programmable. That means rules can be baked directly into the money itself.

Governments could set expiry dates on your balance to force you to spend it. They could restrict purchases of specific goods. They could limit how far from your home you're allowed to spend. None of this is tin-foil hat territory.

Programmability is openly discussed in central bank working papers as a benefit. India's RBI is already testing programmable payments that restrict how government transfers can be spent.

The ECB has talked about putting holding caps on the Digital Euro. China's system already limits wallet balances by tier.

Once you accept that money can have rules attached, the question stops being "will they?" and becomes "how far will they go?"

The Freeze Button

Your bank can freeze your account. It's annoying, there's paperwork, and there are legal protections. With a CBDC, the central bank could do it directly. Fewer steps. Fewer safeguards.

Canada gave us a preview in 2022 when the government froze bank accounts of trucker convoy protesters and their donors. That required coordination with commercial banks and generated massive backlash. A CBDC would make it frictionless. One click. No intermediary needed to comply. No commercial bank to push back or drag its feet.

If you're comfortable with the current government having that power, ask yourself if you'd be comfortable with every future government having it too.

Banks Get Squeezed

This one's less about your privacy and more about how the whole system changes shape. If people can hold money directly with the central bank, why keep deposits at a commercial bank?

That's not a hypothetical concern. It's why the ECB is capping Digital Euro holdings and refusing to pay interest on them.

They know the risk. If enough deposits migrate from commercial banks to CBDC wallets, banks lose their funding base. Less funding means less lending. Less lending means credit decisions start shifting toward whoever controls the CBDC infrastructure. Which is the government.

China sidestepped this by turning the e-CNY into a bank deposit product. Clever. But it still runs on state-controlled rails, and the central bank still writes every rule.

CBDCs vs Cryptocurrency: Same Screen, Different Universe

They're both digital. They both live on your phone. That's roughly where the similarities end.

Crypto was born out of distrust. Satoshi's whitepaper dropped in 2008, right as banks were collapsing and governments were printing money to bail them out. The entire point was to build money that no single entity could control, censor, or inflate on a whim. CBDCs are the state's answer to that same moment. Same problem, opposite conclusion.

Crypto said "take the power away from institutions." CBDCs say "give institutions better tools."

Bitcoin has a hard cap of 21 million coins. Nobody can change that. Not a CEO, not a president, not a committee. A CBDC's supply is whatever the central bank decides it is on any given Tuesday.

Bitcoin transactions are pseudonymous. Privacy coins like Monero go further and make them fully untraceable. CBDC transactions are visible to the issuing authority by design.

Nobody can freeze your Bitcoin ( If you hold your own keys). You control it. A CBDC account can be frozen, restricted, or programmed with spending conditions without your consent.

Crypto doesn't care about borders. You can send Bitcoin from Bangkok to Buenos Aires at 3 am on a Sunday, and nobody needs to approve it. CBDCs are jurisdictional by nature. The Sand Dollar is restricted to domestic use only. Most CBDC designs are built the same way.

Feature | CBDCs | Crypto |

Issued by | Central bank | Decentralised network |

Control | Centralized, state-run ledger | No single entity is in control |

Privacy | Full state visibility | Pseudonymous or fully private |

Supply | Unlimited, set by policy | Capped, fixed by code |

Censorship | Accounts frozen with one click | Resistant by design |

Legal tender | Yes, mandated | No, treated as a digital asset |

Volatility | Pegged to fiat | Market-driven |

One system extends the state's reach into every transaction. The other was built specifically to make that impossible.

Can They Coexist?

They already do. And probably always will.

Governments aren't going to abandon CBDCs. Too much money spent, too much institutional momentum, too many policy goals tied up in them. China's not walking back 3.48 billion transactions. The EU isn't scrapping years of Digital Euro prep work. These projects have their own gravity now.

No Masters

But crypto doesn't need government approval to exist. That's the whole point. Bitcoin kept running while China banned mining. It kept running while India tried to tax it into irrelevance. It kept running while the SEC spent years trying to regulate it out of polite society. Permissionless means permissionless.

Some countries will push CBDCs on their populations. Others will ban them. Most will end up with some awkward middle ground where both exist, and regulators spend decades trying to figure out how they feel about it. Crypto doesn't wait for that process to finish.

The Stablecoin Question

Stablecoins sit in the weird space between both worlds. Dollar-pegged, digitally native, but issued by private companies instead of central banks. And governments have noticed.

China's e-CNY 2.0 upgrade was explicitly positioned as a competitor to stablecoins. The PBOC's deputy governor said it directly. The US went the opposite way, passing the GENIUS Act to encourage regulated private stablecoins while banning government-issued digital currency.

The EU's Digital Euro comes with holding caps designed to stop it from competing with bank deposits. Tether, meanwhile, posted $13.7 billion in profits for 2025. The private market isn't waiting around for central banks to get organized.

Stablecoins might end up being the bridge, the battleground, or both. Either way, they've made the old "crypto vs CBDC" framing too simple. There are now three players on the field.

Your Money, Their Rules

We've tried to be fair here. CBDCs aren't pure evil. But the track record so far isn't encouraging.

The countries that have launched CBDCs are struggling with adoption. The countries pushing hardest are the ones with the worst records on personal freedom.

And the design features that make CBDCs useful to governments (programmability, surveillance, freeze capabilities) are exactly the features that make them dangerous to everyone else.

Crypto exists because someone asked a simple question: What if money didn't need permission? CBDCs exist because governments asked a different one: what if we never had to ask?

If You Care About Control, Start With Knowledge

LearningCrypto gives you live on-chain analytics, an AI copilot pulling verifiable data, and a community focused on fundamentals, not hype. Join the Classroom on Discord. Track smart money. Build knowledge that holds when markets move.

FAQs

Will CBDCs replace cash?

Not overnight. Most central banks say CBDCs are designed to complement cash, not replace it. But actions speak louder than whitepapers. Sweden started exploring the e-krona specifically because cash use was disappearing. Nigeria pushed the eNaira while simultaneously restricting cash withdrawals.

The pattern tends to be the same: introduce the digital option, then slowly make the physical one harder to use. Whether that's replacement or retirement depends on how generous you're feeling with the terminology.

Can you use crypto to avoid CBDCs?

Technically, yes. If you hold your own keys on a non-custodial wallet and transact peer-to-peer or through decentralized exchanges, you're operating outside the CBDC system entirely. But if your rent, taxes, and salary all run through a CBDC, you'll still interact with the system whether you want to or not. Crypto gives you an exit, not a forcefield.

What's the difference between a CBDC and a stablecoin?

Both are pegged to fiat currency. Both are digital. A CBDC is issued by a central bank and comes with full government oversight, transaction visibility, and whatever rules the state decides to attach. A stablecoin like USDT or USDC is issued by a private company, runs on public blockchains, and operates outside direct government control. One is state money gone digital. The other is private money trying to stay stable.

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Hard Money Brief

Free Every Week

Secure your edge: Get Crypto Made Easy PDF + weekly insights—free today.

No spam, unsubscribe at any time. By subscribing, you agree to our Privacy Policy. Need to unsubscribe? Unsubscribe from newsletter.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Cryptocurrency investments carry risk; you should always do your own research before making any investment decisions.

Heidi Chakos is co-founder of LearningCrypto and creator of the @cryptotips YouTube channel. A cryptocurrency educator and author with over a decade in the space, she specialises in Bitcoin fundamentals, self-custody, and on-chain analytics. Follow her on X at @blockchainchick.

View all articles →